We’ve been getting calls these days from folks who have been injured in crashes asking about things they’ve learned from ChatGPT or other AI-based sources. They are asking questions like:

What should I do after my bike crash?

Do I have a claim? How do I know?

How do I present a claim?

Do I even NEED a lawyer?

And, of course, the Big One: WHAT’S MY CLAIM WORTH?

Perhaps it is time for a bit of a Primer on these issues!

CLAIMS ARISING OUT OF A BIKE v CAR CRASH

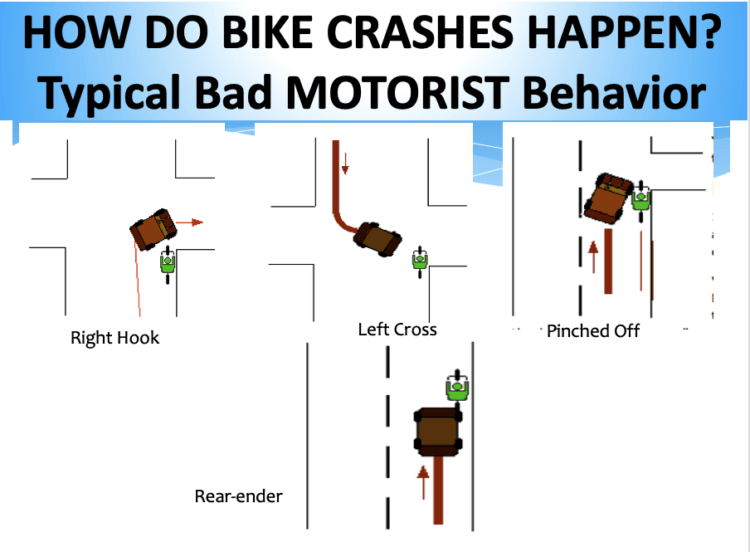

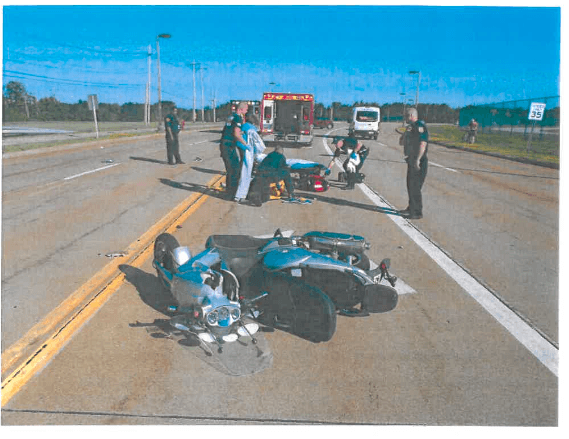

You were riding along on the road and got whacked by a motorist. You were, you thought, doing everything right and the motorist, you believe, screwed up and hit you. This probably occurred in one of the four most common Car/Bike Crash scenarios: Right Hook – Left Cross – Rear Ender – Passing/Pinched Off

Assuming you were doing everything right, and the motorist did something wrong and hit you and caused you to be injured then, at that very moment, a new “CLAIM” was born. This claim is a “thing” – it’s YOUR thing. It belongs to YOU. This claim has some “value” – money value – but only in a very special marketplace and only to one very special person/entity- the insurance company for the person who hit and hurt you. At some point in the future, this insurance will want to buy your claim from you. The insurer wants to pay THE LOWEST POSSIBLE PRICE to you, just like the person who buys your used car wants to pay the lowest possible price for your car.

Does this mean the insurer is “Bad” for not paying you what you want? No, the insurer is a Business and YOU are a NUMBER to them. They want to maximize profits by minimizing what they pay out in claims. The insurer has trained its representative and adjustors to seek out and highlight all the factors in your claim that they can use to diminish the value then argue with you until you submit to their way of viewing your claim.

In a claim of any real value, YOU should have someone on YOUR side who is trained to deal with the insurer- and trained to MAXIMIZE the value of your claim by developing the claim in such a way that the value is clearly seen.

I have had this lithograph – “The Advocate” – in my office since the early 1980s – I’ve always carried this idea of the Lawyer for the victims fighting for Justice & shielding his clients from the aggressive tactics of folks coming at him or her… that’s what we do in these Bike Cases – we understand the process – we understand what factors give your claim value – we how insurers “think” – we understand how to present the facts, data, medical evidence and pain and suffering to the insurer in such a way as to cause the insurer to pay the most it will pay, and then some, to “buy” your claim from you. And…if the insurer balks at paying a fair price to buy your claim, we have the skillset needed to get your case into the court system and take it to trial if necessary.

THE CLAIMS PROCESS

I’ve been handling “insurance claims” for over 40 years now. Despite all the changes the world has seen, the basic claims process has not changed much. A claim is opened – data from the crash, injuries and such are provided to the insurer – the data is analyzed and the insurer develops its view of the value of the claim. They are experts at this – and experts at MINIMIZING their exposure and pay out. My job is to present the claim in the best possible light – counter any arguments they have on claim and get the insurer to pay out a sum that is…uncomfortable… to the company – to get every dime they want to pay, and then some.

The “claims process” starts the moment the insurer is notified about the crash. The insurer opens a new claim, assigns that claim a unique Claim Number, assigns a Claims Rep or Adjustor to handle the claim, and immediately starts going through its protocol for gathering information to assess the claim.

How does the insurer find out about the crash. Well, a “good” motorist notifies the insurer – tells the insurer “Hey I screwed up and caused a crash and hurt somebody on a bike.” But… that often does not happen. Just this week alone I have contacted three different insurance companies to open a claim because the At Fault driver failed to notify their insurer.

When a person hires us to handle their injury claim we immediately have a lengthy Day 1 To Do list – We will FULLY investigate the claim-gather all police records/photos/video – get all witness statement- get Cruiser/Body Cam – 911 calls – security video- Toxicology or other Forensic reports- get any crash reconstruction data, Black Box data, Measurements – TALK to witnesses – LOOK FOR other security cam or Doorbell cam footage – Think about whether this is a case where a Crash Reconstruction Expert is needed – would the Black Box in the car yield any important data? If so, we may need to file a lawsuit on Day 1 and secure the data with a Temporary Restraining Order.

We will also notify the driver, and their insurer of the crash, your claim & our involvement. We’ll send a Notice to Preserve Evidence, demanding that any cell phone and other data in the car be preserved… the phone itself, any data ON the phone and all the billing records.

We will demand that the CAR and its Black Box be preserved. We typically cannot “GET” that phone/black box data without a subpoena but… we will put the driver on notice that they must preserve it. If they don’t preserve the data they could be a risk for another claim for “spoliation of evidence.” Also, if they’ve been told to preserve, say, their cell phone & its data/messages, etc and, when asked about it during a deposition they say “oh… that phone broke, so I got rid of it…” it can sound VERY shady to a judge or jury…

We will want the driver to notify the insurer. Today, the investigating officer in Ohio is SUPPOSED to check and confirm insurance coverage for the driver… sometimes they do that – sometimes they don’t. The LEO is also SUPPOSED to put the insurance company & policy number in special boxes on the crash report and… Ta Da… sometimes they do that and sometimes they don’t. Frankly, we seem to see Police take a more lackadaisical approach to crash investigation when cyclists are the victim. Sometimes we have to fight with the victim just to get the name of their insurer…

The initial communications with the insurer are VERY important. What you tell, or don’t tell, the insurer Day 1 can impact how easy or hard it is to resolve the case on Day 400. Our initial communications & correspondence with the insurer is both Tactical and Intentional.

When I was an in-house lawyer for an insurance company I definitely learned how important those communications are and I try to use those lessons when dealing with the assigned adjustor. In the “Olde Days” when I was a young lawyer using a quill pen to write to the insurer on parchment, insurance adjustors were almost always aggressive, angry, overworked, obnoxious older men who would belittle the lawyer and her/his client from Day 1 until the day they cut the settlement check. Not so much any more. Still, it helps to communicate effectively and develop a rapport through honest and open discussions with the adjustor.

[Oh…and I STILL use a very nice fountain pens to sign letters, printed on our letterhead]

When we get a case we handle everything – all communications – all data gathering – we obtain all medical records from all of your treatment – we obtain all the bills – we think about whether medical experts might be needed in a severe injury/TBI case.

Your job is simply… to get better. And to keep us in the loop so we can order all the bills and records we need to present your claims. When you’re all better we will put all the data into one big package – The Settlement Demand Package. I review every piece of better, every medical record and bill. I put it all into one fairly lengthy letter to the insurer that outlines the Liability & Damages facts: the crash, injuries, treatment, pain and suffering. At the end we ask for a dollar amount called our Opening Demand.

The BIG Question everyone has is: “What’s My Claim WORTH?”

The answer is… Ta Da … complicated… but nobody on planet Earth can give you that answer on Day 1. The “Value” of an injury claim depends on… Ta Da… the nature and extent of the injuries, the treatment, the medical bills, and many other factors that NOBODY knows on Day 1. It also involves WHERE the crash occurred. Claims in NYC are going to be valued differently than claims in rural Ohio.

Ohio is an interesting jurisdiction. We are the 7th largest state. That fact surprises a lot of folks. There are almost 12 MILLION people in Ohio. We lack the superHugeMega City like NYC or LA or Chicago or Houston but we have several good sized metropolitan areas, along with a lot of rural space. Ohio has 88 counties and I’ve had cases in many/most places here. I just filed a lawsuit in Van Wert County, my first time there. The same crash case likely has a different value in West Union than it does in Ashtabula or Toledo or Bellefontaine or Marietta! It takes some experience to figure that out.

I found this cutting board, an Ohio map, and marked some of the spots where I have handled injury cases, mostly Bike cases, but also car, truck, and motorcycle crash cases.

Having said that, I think I can pretty well gauge the numbers of 0’s in your claim value pretty early in the process. Is your claim value from $10,000 – $99,000 or “Six Figures” or beyond? If you have the right background and experience, this is are difficult to see fairly early in the game for the most part.

Why?

Well, I’ve handled 1000s of injury claims from Day 1 to Settlement – Day 1 to Trial & Verdict – Day 1 to Trial & Appeal. I’ve worked with all types of clients and insurance companies. Following trials, I’ve talked to juries about why they evaluated claims the way they did. I’ve been involved in mock juries. I’ve researched & written & presented seminars to lawyers & judges about jury verdicts and the factors lawyers listed that led to the verdict.

Also, I handle bike cases through, usually, a “Contingent Fee” agreement. What does THAT mean? Well, that means I ONLY get paid if we are successful & there is money in the bank. My fee is a percentage of what we are able to collect. We also advance costs, which means I basically pay, up front, the case expenses, hundreds, or even thousands of dollars. We get reimbursed at the end.

When I went out on my own I learned very quickly that if I made a mistake on Day 1 – took in, worked up, and spent hours and hours developing, a case that turned out to be a loser, or which had a value less than I thought then… well… I didn’t eat. The Contingency Fee means the client NEVER GETS A BILL. The lawyer takes the risk and spends time & money and may never get paid. I learned VERY QUICKLY to get really good at Picking The Winners on Day 1!! That meant learning to evaluate the Big 3 – Liability – Damages – Insurance – early in the case and to get it right.

So, in addition to “Big” damages and injuries, we look at a several other things on Day 1. First, “Liability” – who is at fault and why? How easy/difficult will it be to prove liability? Is the client telling me the truth – do the facts make sense? Does teh client tell the story effectively? Do they come across as truthful or does it seem like they are trying to make a mountain out of a molehill?

What does the police report say? This is certainly NOT determinative. As noted, police often side with the motorist over the cyclist. But, if the police are against you, it is a hurdle. We are very good at getting over those hurdles in the right case, but it is something we look at on Day 1.

So with Liability and Damages, the third thing we look for is, of course … INSURANCE! Does the driver have auto coverage? Does the client have an auto policy and/or excess coverage?

Can you go after a driver who is uninsured? Sure… but… it usually doesn’t make much financial sense. MOST people, if you turn them upside down & shake them, have more Debt than Cash. Most people can’t afford to pay any type of injury claim. If you do go after them, sue them, spend the time & money in litigation, go to trial and win a nice judgment, they can just file Bankruptcy and make the debt go away! It’s almost NEVER a good idea to take this route. THAT is why protecting yourself with good Auto/UM/Homeowners coverage is so important!

If you have a “big” claim – six figures and beyond – then you have significant, serious injuries and losses that were, typically, immediately recognized as such. You likely had injuries that were debilitating – that prevented you from working – that have some element of permanency. Your losses are substantial.

Big” claims like that are pretty easy to spot on Day 1 and Big Claims require LOTS of BIG WORK by good lawyers. Do NOT try to handle a claim like that by yourself. You simply lack the skills to do so, and, frankly, you are probably too close to the pain to evaluate the claim fairly. You should ALWAYS get a good Bike Lawyer involved in a claim involving serious injuries.

Some lawyers only want to handle “big” claims but MOST car/bike crash claims out there are in the “five figure” range, not the six figure range. The cyclist is hit and gets hurt – often seriously hurt – and they work hard to get better. They get treated at the E/R – follow up with their Primary Care doc – get sent to a specialist or maybe to Physical Therapy. Our cycling clients are unique in that THEY WORK HARD at getting better- they treat their therapy like a big hill – sometimes the docs have to say “Slow Down” but by and large cyclists get better, and get better faster than the medical team expected. These can still certainly be very serious claims and this category of claims probably makes up the bulk of the claims we see in our statewide practice.

When we take a case we will ask YOU some important fact questions about what YOU were doing. Were you actually on the ROAD, and not the berm, shoulder, sidewalk, tree lawn. What were the light conditions? Weather? What were YOU doing? Did you have your hands on the handlebars? Engaged in any “trick” riding? Riding “with” traffic, not against traffic [hopefully]. What lane were you in? Does that even matter? [Narrator: it MIGHT…] Where in the LANE were you? Does that even matter? [Narrator: It MIGHT…] Were you turning? Preparing to turn? Did you SIGNAL a turn? Does that even matter? [Narrator: It MIGHT…] What was your speed? What gear were you in? Did you use/wear anything to make yourself more conspicuous? Flashing lights- bright colors. Is that even REQUIRED by The Law? [Narrator: NO but… if you were in “dark” clothes it will likely be noted in the crash report]. Were you wearing a Helmet? Does THAT even matter? [Narrator: No… well… maybe… ] Did you take any evasive action? Does that even matter? [Narrator: well… maybe…]

The “Insurance” we’ve been talking about so far has been the auto coverage that, hopefully, the driver who slammed into carries…but…

A/ Not all drivers are insured and

B/Not all drivers have ENOUGH insurance to pay your claim.

In Ohio, the “State Minimum” level of auto coverage is $25,000.00. That means a driver can “stay legal” as long as they carry an auto insurance policy with $25,000 in “liability” coverage… i.e., coverage that applies to crashes they cause. $25,000.00 is … not good. It is VERY easy to a routine post-crash hospital trip to the E/R to cost MORE THAN $25,000.00, let alone follow up care and treatment. By the time you add in wage loss, other out of pocket expenses, and your pain and suffering, that $25,000.00 policy is basically a down payment.

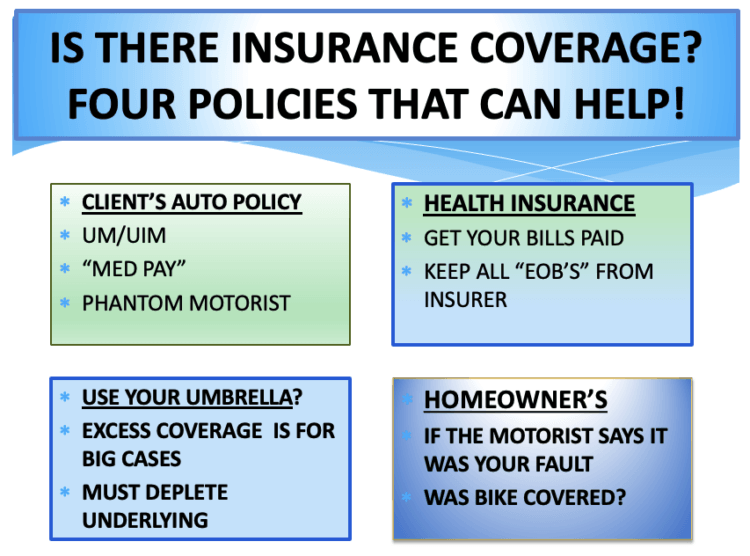

In my Bike Law 101 classes for lawyers & judges, I find that MANY lawyers are surprised to learn that a car/bike crash can trigger coverage and claims in FOUR or more insurance policies.

Say WHAT?

Yep. In addition to the other driver’s auto policy, we will dig into YOUR health insurance, YOUR auto insurance, YOUR homeowners insurance and YOUR umbrella or excess coverage. This is a slide from my BIKE LAW 101 Seminar.

YOUR HOMEOWNERS?

OK, I give up – how does your HOMEOWNERS policy come into play when a car slams into you while you are on a bike ride?

Well… there are actually TWO ways the H/O policy can come into play. We handle bike cases for many riders who spend… a LOT… on their bikes… like… a LOT [You KNOW who you are]. They spend so much that often insurance adjustors, who don’t get a lot of “car slams into expensive bike” cases, are shocked that we are submitting a claim for $5,000 or $10,000 or $15,000 … for a BIKE? The auto carrier will often nickel and dime us on these property damage cases [do Kids These Days even know what nickels and dimes are? But I digress…]

Cyclists often don’t realize that their bike is covered by their Homeowners policy. When they are struck by a car, they can present a claim to their H/O insurer, NOT their car insurer, for their property damage! We find that the H/O insurer often treats its insured, the cyclist, more fairly than, say, the offending driver’s auto carrier and we can get a better payout under the rider’s “replacement cost” coverage through the Homeowners coverage than we can through the other party’s auto coverage. Your H/O carrier will then go after the other insurer for reimbursement and, because it was NOT YOUR FAULT, they payout will not “count against you” or jack up your premium.

In addition to the bike, all the other expensive toys cyclists use are covered – watches, Garmin, Shoes, Jersey, Helmet, Glasses, etc… But DO NOT GIVE UP YOUR HELMET OR BIKE TO ANYONE. Sometimes the helmet company will say “Give us the smashed helmet & we’ll replace it for free!” Do NOT do this – that helmet is valuable evidence in your case. The Helmet Company is NOT being “nice” – they are taking potential evidence of a claim against THEM for a defective helmet out of the picture.

Sidenote: This H/O approach works for car/bike crashes, but would also work for, say, a dog attack where the bike was damaged. However, UM Coverage ONLY works for AUTO/Bike crashes. If a dog causes your injuries and the dog owner has little or no insurance you are out of luck…

The second way your H/O policy can be used is if the motorist claims the crash was YOUR fault and comes after you for damage to their car. The “Liability” coverage of your H/O policy is there to protect you. If you get sued, your H/O insurer will hire counsel to protect you.

I’ve had several cases, mostly involving folks who ran into my cycling clients with motorcycles, where we have used the cyclist’s H/O policy this way. The cyclist hires me to handle their claim against the other side. The other side sues the cyclist. We notify teh H/O carrier who assigns a lawyer to defend the lawsuit. I then work with that lawyer – we share costs and data throughout the litigation. When I file a counterclaim against the other driver, they notify their carrier and they get a lawyer to defend the claims I brought. So now we have 2 parties and FOUR lawyers… sheesh…yes, it can get messy…

YOUR AUTO POLICY

Your auto policy has TWO coverages that might come into play. First, you probably have “Medical Payments” coverage. This is usually a smaller number – $1000 or $5,000 or $10,000 typically. I’ve seen $25,000 and even $100,000 policy limits in “Med Pay” coverage but that is pretty rare. This Med Pay coverage is like a mini-health insurance policy inside the auto policy. If YOU are involved in a “car crash” then this money is available to help YOU pay YOUR medical bills. This applies even if you are NOT IN A CAR. So if you are hit by a car while riding your bike, Med Pay applies. If you are standing at the bus stop and car hops teh curb and hits you… Med Pay applies. If you are sitting in your bedroom on the 2nd floot watching TV and a car comes flying in and hurts you… Med Pay applies.

In today’s world, with high deductibles and clients who lack significant savings to pay unexpected medical bills, this Med Pay coverage can be a pot of gold. You are hit by a car and your deductible isn’t met so you now owe $4500.00 to the E/R that treated you. We can often tap into your auto policy’s MED PAY coverage to get that paid.

Another typical coverage in the Auto Policy you may need to use is the “Uninsured/Underinsured Motorist” coverage. Again, this applies when the OTHER DRIVER is uninsured or underinsured [lacks sufficient coverage to pay your claim]. This UM/UIM coverage applies even if you were NOT IN YOUR CAR.

We URGE, STRENUOUSLY URGE, all cyclists who ride on the roads to think about buying as MUCH UM/UIM coverage as they can afford. It’s pretty cheap and can be a Life Saver when the idiot who slammed into you says “Oops, forgot to pay my premium and they canceled my policy…”

YOUR UMBRELLA/EXCESS POLICY

Umbrella Coverage or “Excess” coverage is an additional policy you can buy. It is very cheap – and it ONLY comes into play when all of your OTHER coverage is used up. So let’s say you are in a big crash and have a big case but the other driver has no insurance. You have $250,000 in UM/UIM coverage [YAY!], but the value of your claim is a lot more, say, $500,000.00 [BOO!]. If you have a $1.0 million “Umbrella” then that Umbrella can be used here because the $250,000 is insufficient to pay the claim. So even though the other driver had NO insurance, you can use the $250,000.00 from your UM/UIM and then another $250,000.00 from your Umbrella policy to receive the full $500,000.00 value of your claim.

Again, if you are on the ROAD a lot we URGE, STRONGLY URGE, you to get both UM/UIM and UMBRELLA Coverage… just make sure your umbrella doesn’t “…have a hole in it…” You can read about THAT issue here…

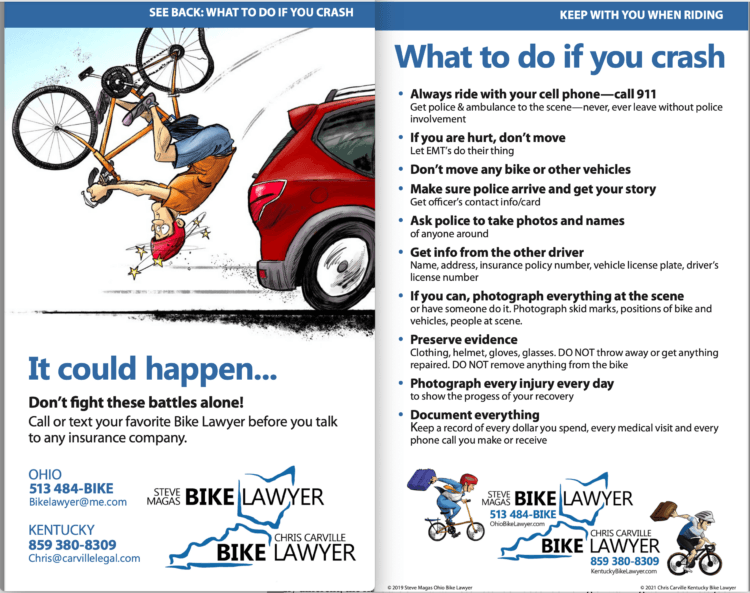

So… you got hurt in a crash… What should YOU do? Well, thankfully, there’s a handy dandy 4×6 glossy card we can send you that talks about that… Just send me an email at Steve@OhioBIkeLawyer.com and tell me A/How MANY you want and B/ Where to send them and we’ll get them out to you. I can send 10 or 100 or 1000 if you REALLY have a lot of friends, or are running a big event!

You don’t have to work through ALL THIS STUFF ALONE- Our job is to handle claims – give us a call and we’ll tell you what we think!