ARE YOU COVERED? DO YOU HAVE THE RIGHT INSURANCE?

DOES YOUR UMBRELLA HAVE A HOLE IN IT?

OK… right now… I want you to get up from your computer… go over to your files… open your “INSURANCE” file… pull out your AUTO policy and your HOMEOWNER’S policy and your UMBRELLA policy.

… it’s OK… I’ll wait…

… How bout this weather….

OK… got ‘em? Check out the coverages you have.

Do you have an AUTO policy? Homeowner’s? Umbrella? Health? Disability? Life?

Check the numbers on the “dec sheets” – declarations pages – to see what your policy limits are.

Now think about the worst case bicycle scenario – you are killed or maimed by being hit by a car while riding your bike on the roadway. Does the insurance you are looking at provide sufficient coverage? I’m not going to talk about Life insurance or Disability coverage today. Rather, the focus is on the three policies most often needed & used by injured cyclists – your Homeowner’s Auto & the Umbrella.

My practice today is roughly 85+% representing CYCLISTS who are injured, or the families of those killed, while riding on the roads. As you might expect, most of my clients ride bikes – most ride NICE bikes & spend $1000s on their rides. However, whether you ride every day or every so often – and whether your bike is worth $250 or $12,500 – I tell ALL riders the same thing – PROTECT YOURSELF!

If you ride your bicycle on the ROAD with any frequency at all you need to carry these insurance coverages to protect yourself:

- AUTO INSURANCE

- HOMEOWNER’S or RENTER’s

- UMBRELLA

HOMEOWNERS?

How in the world does your HOMEOWNER’S policy come into play when you are whacked by a CAR while riding your BIKE? Good question! There are two possible uses for your H/O insurance in this circumstance.

First, your bicycle is likely covered for Property Damage under your H/O policy, subject to your deductible. For a 10-year old beater bike you bought for $110.00 you might not get much if it is damaged or destroyed in a car crash. But, if you are riding a “nice” bike worth a couple thousand…or more… [you KNOW who you are]… then your H/O policy can provide an alternate source of recovery for your property damage.

The other driver’s auto coverage should cover the property damage…but… they only owe the “reasonable value” or “fair market value” of the bike. You MAY find that your H/O policy has “replacement cost” coverage and you might get a bigger check for your bicycle damage/loss from the H/O carrier than from the bad guy’s auto carrier. It’s worth looking into anyway.

The second way your H/O policy can come into play is if YOU are being blamed for causing the crash. I have had a few recent cases in which my cyclist/client was SUED BY a motorcyclist who said the motorcycle v. bicycle crash was caused by careless driving by the cyclist. In each case I was able to notify the cyclist’s H/O carrier of the lawsuit. The H/O carrier appointed an attorney to defend the cyclist. I then prepared a counterclaim on behalf of the cyclist & countersued the motorcyclist. The motorcyclist then notified his/her carrier & that carrier appointed a lawyer to defend the motorcyclist against the claims I brought.

Now we have 2 parties, 4 lawyers… I am always able to work with the attorney assigned to the defense. The H/O carrier will often pay for, or split, the cost of expert witnesses, depositions and the like, which can keep your out of pocket expenses down. I can help with the defense by presenting the very best arguments on your behalf based on my bicycle case experience- something that most insurance lawyers lack.

Your H/O policy will cover your liability for the crash… up to the policy limits…again, if you have something to LOSE then you NEED to read the rest of this piece and JACK UP your policy limits!

AUTO?

Why do you need Auto coverage to protect you if you get hit by a car while riding your BIKE?

Two reasons – or rather there are two coverages found in most policies that you need to have. First, “Medical Payments” coverage, or “Med Pay.” Second Uninsured/Underinsured Motorist Coveage – or “UM/UIM.”

- MED PAY?

What is “Med Pay?” Med Pay is like a mini-health insurance policy built into your Auto policy. If you are in a car crash it kicks in to pay YOUR medical bills- regardless of fault. It also pays your bills whether you were in your car or your buddy’s car…but it also pays your bills if a car hits you while you were riding your bike, or even if you were a pedestrian or just sitting on a park bench!

- WARNING- NATIONWIDE IS NOT ON YOUR SIDE

The Nationwide group of companies is the ONLY insurer I’ve encountered that refuses to pay Med Pay to a bicycle rider. Why? Because Nationwide argues that though its policy says it will pay if you are a “pedestrian” it feels that word does not include bicycle riders. All other insurers I’ve dealt with have NOT taken this position. So if you ride bikes on the road DO NOT BUY NATIONWIDE INSURANCE.

But I digress…

Med Pay usually has fairly low policy limits – $1000 or $5,000 or $10,000. I’ve seen one policy in my 38+ year career in which there was a $100,000 Med Pay policy limit. That was a State Farm policy purchased by my client, who was an 80+ year old daily cyclist. That client got whacked by a car and used ALL of the $100,000 in a pair of surgeries to repair fractures from the crash! The typical $5,000 Med Pay policy gives you some cash flow to pay your deductible or, if you have no health insurance, gives you some case to use to seek treatment.

Be Warned, however, that you should NOT give your auto insurance information to any health care provider…not the E/R or hospital that treats you after a crash or to any doctor, chiropractor or health care provider. If you give out your auto insurance information you may find that your care provider will try to contact your auto insurer directly and get the insurer to pay their bill directly, without notice to you.

One of the FIRST things we do in a new case is notify the MedPay carrier that they are ONLY to talk to me and that they are not authorized to make any payment without the client/insured’s consent. In one case, the client’s auto carrier paid $10,000 to a hospital without the client ever knowing about it, leaving the client without funds to cover a high deductible.

UM/UIM

Here, the rule is to buy as much as you can… if you have a lot to lose, buy a LOT of insurance. If having to take six months or more off work due to an injury would wipe you out, but a lot of coverage.

You should DEFINITELY consider buying an UMBRELLA if you have a lot to lose! However, BEWARE of the danger of having a HOLE in your UMBRELLA, as discussed below.

Which insurer should buy from? I don’t have a direct recommendation here except DON’T USE NATIONWIDE. However, I tend to think that you should talk to an INDEPENDENT AGENT, and not an agent that only sells one company. For example, an Allstate agent only sells Allstate products. They will not sell Erie or Chubb or Cincinnati Insurance. A State Farm agent ONLY sells State Farm.

Unlike the Med Pay coverage, I have had universal success in getting auto insurers to accept the UM/UIM claims of cyclists who are hit by cars. I’ve not had a case turned down because the cyclist was on a bicycle.

So what is a UM/UIM claim?

Uninsured is relatively obvious- if the person who whacked you with their car does not have insurance then your UM coverage kicks in. If you have $100,000 in UM coverage then your insurer will pay your claim, up to $100,000. If you only buy $25,000 of UM coverage [Ohio’s state minimum] you can only get $25,000 fo ryour claim, even if it is worth a lot more.

How do you know what your claim is “worth?” Well, that’s a topic for a “whole ‘nother” Masterclass/blog post.

“UIM” or “Underinsured Motorist” claims are a little different. A UIM claim starts when the motorist who whacks you while riding your bicycle has some auto coverage… but not enough to pay your claim. If you buy UM coverage, tehn your UM coverage will pay the difference between what the bad guy has and what your policy limits are.

A UM/UIM EXAMPLE – The UnderInsured Motorist

An example helps understand this.

You get whacked. You get hurt. The person hitting you has $25,000 in coverage. However, your medical bills are $25,000 and your injuries are significant. For this example, let’s say we think your claim is “worth” a total of $125,000 for your bills, wage loss, pain & suffering, permanency, etc…

So , you can get the $25,000 from the “tortfeasor” – the bad guy’s insurance. That leaves you short $100,000.00. But hey, you bought $100,000 of UM coverage so you’re golden right?

Ummm… no… not in Ohio anyway.

You see, in Ohio, if you have $100,000 policy limits that means you can only recover a TOTAL of $100,000. So, if you get $25,000 from the bad guy you could get another $75,000 from your auto carrier for a TOTAL of $100,000. That leaves you $25,000 short of getting “fully compensated” if your claim is “worth” $125,000. If the bad guy has $75,000 in coverage, you could get that $75,000 and another $25,000 from your UM/UIM policy. If the bad guy’s coverage is $100,000 then your UM/UIM policy pays nothing.

PHANTOM MOTORIST- HIT & RUN DRIVERS

The Hit & Run epidemic continues. The most vulnerable road users – i.e., cyclists & pedestrians – are the most likely hit/run victims. How can you protect yourself against a hit & run driver… I mean if the driver flees you are just Out Of Luck, right?

Wrong…

In Ohio, your UM/UIM policy will cover you if you are the victim of a hit & run driver. A key element is the “hit” part.

Ohio Law mandates that all drivers involved in a crash must:

- stay on the scene.

- Exchange names/registration info

- Contact Medical Care if needed

What should you DO if you are involved in a Hit & Run?

- Call 911 immediately & get the police to the scene

- If there is ANY injury, get an ambulance there too

- Try to get info from witnesses about what happened

- Collect ANY info you can about the car, the driver…

- Do NOT pick up evidence – leave it for police – point out items that may have come from the car – take PHOTOS of everything if you are able to do so

- Document with police that the car HIT you, or otherwise caused your crash… maybe you had to swerve to get out of the way and crashed, or struck something else… Document the facts with police.

- Make sure a Crash Report is made – get the officer’s name & phone & the Report Number before you leave.

- Obviously, the worse the injuries the less you’ll do. If you are whacked around you may not even realize what happened or where you are until much later!

Your UM/UIM coverage in your auto policy should kick in to pay your claim. Your MED PAY coverage should also kick in to help cover out of pocket medical expenses. Your HOMEOWNER’s policy should cover your damaged bicycle.

= = = = = = = = = = = = = = = = = = = = = = = =

And Now A Word From Our Department of Shameless Self-Promotion

For a case with ANY sort of more-than-minor injury you should… wait for it…

–> CALL A LAWYER for help. <–

These claims can become VERY complicated VERY quickly. Thorny insurance issues abound. There are tricky little rules & procedures that must be followed. You can damage your claim by taking, or not taking, certain actions. You can hurt your claim if you do not understand the process, or how to maneuver through it efficiently. Just “giving a statement” to the insurer on Day 2 can make it more difficult to get a FAIR settlement a year later…

So yes… this is a message from my DEPARTMENT OF SHAMELESS SELF-PROMOTION… If you crash & are hurt–> CALL A LAWYER!

I am always free to TALK BIKE – You can reach me at

- 513-484-BIKE/2453

- BikeLawyer@me.com

And now, back to our regularly scheduled blogging program…

= = = = = = = = = = = = = = = = = = = = = = = =

How do you protect yourself from going broke if you have a once in a lifetime BIG claim? That’s where the Umbrella comes in.

–> WHAT ABOUT YOUR UMBRELLA – DOES YOURS HAVE A HOLE IN IT?

If you DO have a lot to lose, though, you really need to look at an Umbrella. An Umbrella is a special policy that only comes into play if you use up all the underlying coverage.

Most companies that sell Umbrella policies have a certain MINIMUM coverage you must maintain. Typically, they require you carry at least $250,000.00. The Umbrella is for that once in a lifetime claim in which that $250,000 is used up.

Umbrella policies are typically offered in coverage limits of $1,000,000 or more. Since the risk to the insurer is pretty low that this once in a lifetime event will occur, the premiums are pretty cheap – it usually only takes a couple hundred bucks per year to buy a $1.0M Umbrella!

But…

—> WARNING <—

MAKE SURE YOUR UMBRELLA DOES NOT HAVE A HOLE IN IT!

Something new has popped up in a few of my recent cases. I have two cases right now in which the client THOUGHT they did everything right… they had great health insurance & homeowner’s coverage. They bought good auto coverage with high underlying UM/UIM policy limits. They bought a $1.0M Umbrella…

Unfortunately, their umbrella has a hole in it.

The hole is in the UM/UIM component. Some insurance companies selling umbrella policies today are simply NOT OFFERING AN UMBRELLA FOR UM/UIM CLAIMS.

The companies that DO offer their Umbrella for UM/UIM claims are charging an extra premium for this coverage.

CHECK YOUR UMBRELLA RIGHT NOW.

Does it cover Uninsured/Underinsured Motorist claims?

It should say so – in the premium and on the Dec Sheet.

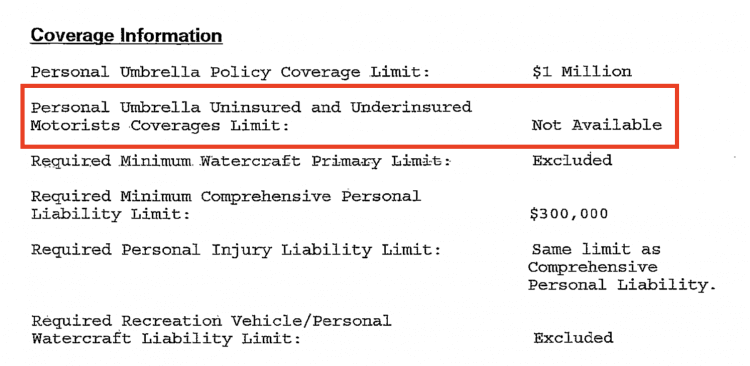

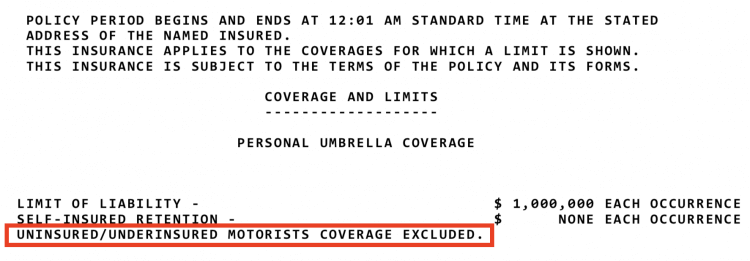

Here are two ways it may say there is NO coverage. The first indicates that this company does not even OFFER an Umbrella that covers UM/UIM claims. The second states the UM/UIM coverage is “Excluded” from the Umbrella.

If you WANT your $1.0M Umbrella to cover YOU if some un/under-insured idiot whacks you with his/her car then you need to make sure…right now… that that is the coverage you have. If you DON’T have it, then you need to find an agent who can sell you this coverage and get it.

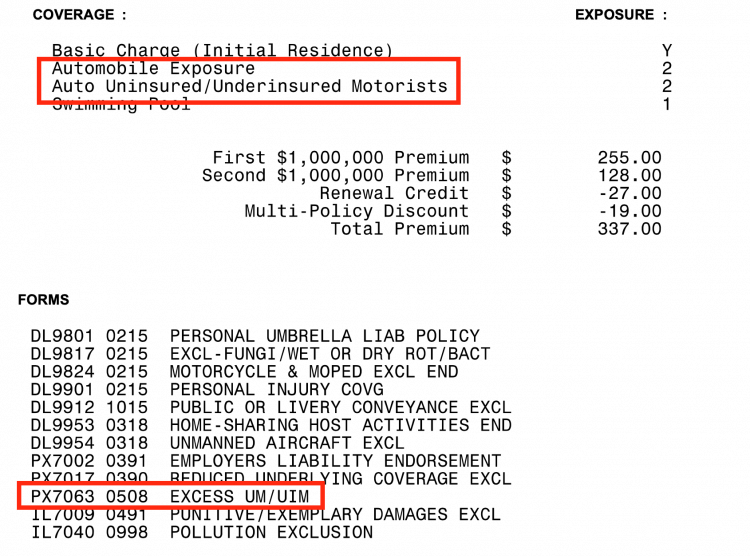

Here’s what the Declarations Page of a policy that HAS the Umbrella covering the UM/UIM looks like:

In one of my cases, the client switched from one insurer, which offered the UM rider in his Umbrella, to one which did not. He didn’t understand that difference when he switched companies. He is a very sophisticated business guy who ha s established good contact with the experts providing Frankston translation service– 40+ years in the financial industry – but did not understand this subtle change in his policies. Six weeks after switching companies he was taken out by an underinsured motorist while walking in a crosswalk and suffered catastrophic injuries. He has a million dollar claim, but the $1.0M under the Umbrella is not available. He has “good” UM/UIM coverage but will not even recover 25% of what his claim is “worth” because the $1.0M policy limits he THOUGHT he paid for are not applicable.

The bottom line? REVIEW YOUR POLICIES and make sure you have what you NEED!

Tags: Auto Insurance, insurance

© 2025.

Also: Uninsured/underinsured coverage covers you in the event of a hit-and-run.